This Week's Deep Dive - tl;dr

The Four Archetypes of Buy-and-Build ("Roll-up") Strategies

Why Most Construction Roll-Ups Fail at Value Creation

The Critical Role of Cashflow Predictability and Market Competition

How Distribution and Go-to-Market Define Success

Real Examples From DTC Aggregators to Constellation Software

Strategic Clusters for Construction Investment Success

I started my career in the M&A arena during the first wave of solar consolidation. Consolidation and buy & build have accompanied my career as an executive, before founding Foundamental, in different ways for my entire way journey.

The first time in my Foundamental capacity that I was triggered by a founder about rollups was in Q2 2021, when I spoke with Philipp at 1komma5grad about their vision (we did not invest for mainly economic and market reasons - too expensive for us to make sense, and we did not and still do not want to be in the solar/PV market - but I believed strongly in him).

The reason I mention this anecdote is that back then, my entire VC friend circle told me “there is no tech to roll-ups, it’s not for us”. And yet, since early 2024, the opinion among many of my venture investor friends flipped like a coin - AI enabled roll-ups for many verticals are suddenly venture backable.

What changed?

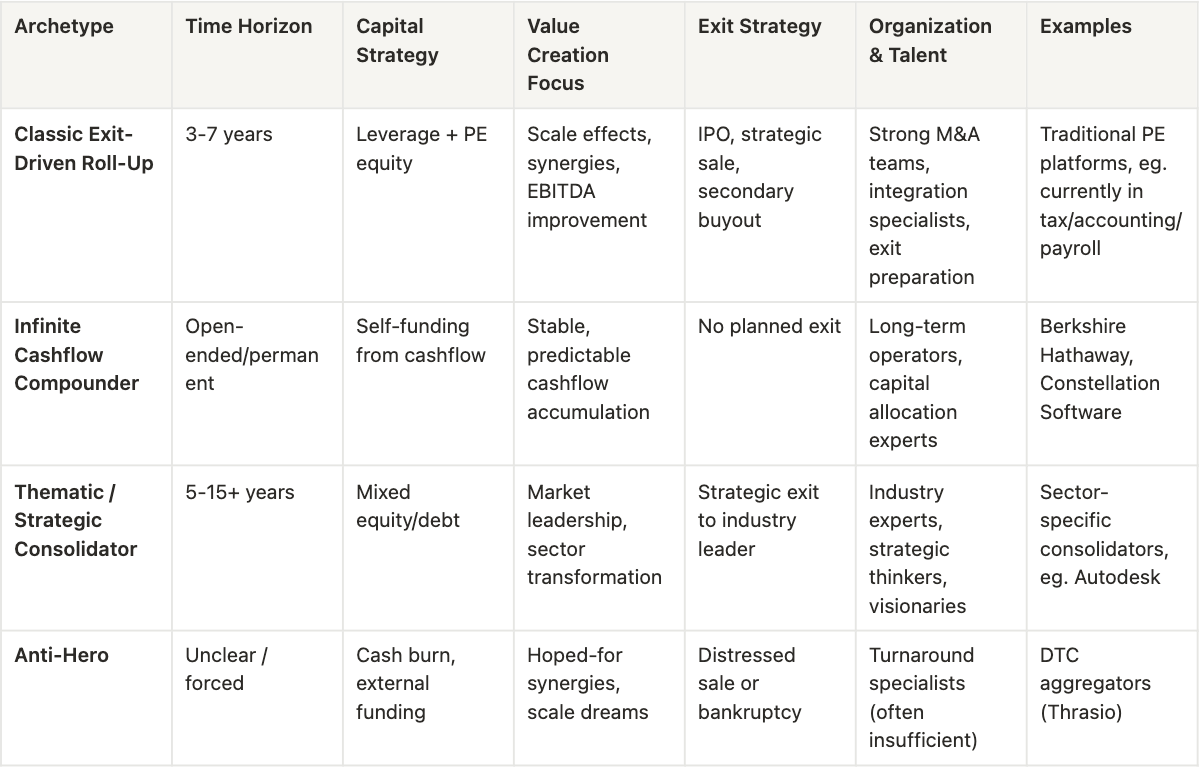

The 3+1 Archetypes of Buy-and-Build Strategies

My colleague Fabio had written his take about roll-ups here. Highly recommended read.

Given my background, I've been doing my own work independent from Fabio, diving deep into roll-up strategies in general, and then looking at them in construction. My aim was, before I get sector-specific, I wanted to understand the fundamental archetypes I observe in successful buy-and-build plays.

Simplifying the world, there are three distinct buy & build models that have worked in specific contexts in the past.

The first archetype is the classic exit-driven roll-up. This follows the textbook private equity playbook. You acquire companies, create scale effects, build a cashflow machine, capture synergies, and deliver higher EBITDA as a group than the sum of individual parts. The end goal is selling this improved group at a better multiple. But from my observation, this strategy absolutely requires a liquid exit market. No liquidity, no strategy. Most traditional private equity platforms follow this model - think KKR's industrial roll-ups or Vista Equity's software consolidations that target 3-7 year exits.

The second archetype follows the Berkshire Hathaway or Constellation Software model. Here you're building an open-ended group, continuously adding more cashflow and using that cashflow to acquire even more cashflow-generating businesses. It's an infinite game rather than a finite one. Private equity roll-up strategies continue to evolve in 2025, with several key trends shaping the landscape, and from what I observe, this compound model is gaining traction.

Constellation now consists of exactly 1000 niche software providers. All were profitable. All were cashflow-positive. They buy extremely niche but dominant and profitable and cashflow-positive companies because this feeds the cashflow of the overall conglomerate.

And then there is the third archetype: the thematic or strategic consolidator. You're not just chasing financial returns or endless cashflow compounding. Instead, you have a longer-term vision to reshape a sector or build strategic market position. You might be consolidating a specific niche market or creating thematic leadership in an emerging area. Examples would include Veolia's consolidation of waste management and water services globally, or how Brad Jacobs built XPO Logistics by consolidating fragmented logistics players with a clear sectoral vision.

The Anti-Hero Archetype - Avoid At All Costs

But it doesn't end here.

The fourth archetype you can observe in the market is our anti-hero. This represents what I believe you should avoid. I call it the anti-hero archetype because it embodies every mistake that destroys value in roll-up strategies.

From my analysis, the anti-hero model has no stable cashflows. You start with unprofitable companies where cashflows are completely unpredictable. You have no solid financial foundation. You choose markets with intense competition and no competitive moats. Customers churn constantly, making it nearly impossible to achieve profitability.

The problem with buying cashflow-negative, burning companies and claiming you'll make them profitable is simple: this energy has to come from somewhere. In the SaaS sector, the product is essentially finished when acquiring. From that point, it's a sales and marketing or distribution game. When you buy cash-burning software companies together that all do different things, your value uplift must come from distribution. So how do you create a distribution advantage?

If you then couple that with a "cross-selling" thesis but you're buying companies that don't fit together, there are no obvious distribution synergies. You end up with a patchwork that can't be properly synergized on the cost item that matters.

And finally, you have no clear exit strategy because the whole thing doesn't present as an attractive package.

Demonstrating The Critical Role of Cashflow Predictability and Market Competition

The DTC aggregator example emerging in 2020-2021 illustrates what I consider this anti-hero model. Companies like Thrasio (bankrupt in 2024) or SellerX built a model to roll up small e-commerce brands operating on thin gross margins. The original thesis seemed sound: buy many smaller brands selling on Amazon, achieve scale effects, optimize logistics, and create a more efficient marketing operation.

But when I apply our success factors to the DTC aggregator example, the weaknesses become obvious. The individual brands had thin margins and were heavily dependent on platforms like Amazon. Cashflows weren't predictable or stable like I'd expect from classic profitable businesses.

The exit strategy was problematic because the overall structure wasn't predictably profitable. Finding a lucrative exit became difficult. Integration proved challenging because the hoped-for synergies were harder to capture than anticipated.

But there's another success factor many missed, and which kept me far away from the solar/PV market for example: capital competition. In markets where many players pursue similar roll-up strategies, it becomes much harder to find genuine bargains or undervalued acquisition targets. When everyone tries the same thing, prices rise and margins get even thinner.

This was exactly what I observed with DTC aggregators. Once the model became known, suddenly many players were doing the same thing. Competition intensified, making it much harder to find good deals. In the lower middle market, where roll-ups accounted for over 80% of all deals, PE drove deal volumes by consolidating fragmented markets, but this level of activity can create its own challenges.

How Distribution and Go-to-Market Define Roll-up Success

Another critical success factor for all 3 successful archetypes: distribution and go-to-market edge.

Consider why tax advisory or accounting firms makes such an amazing buy & build case. Most people think it’s “AI”. No.

These markets work perfectly for roll-ups because customers are incredibly sticky. It's extremely inconvenient to switch from your accounting firm that has dealt with your business for ten years, knows all your historical numbers, and understands your specific situation. Nobody does that. Therefore, you don't need to fix distribution or go-to-market problems with your portfolio companies.

Compare this to property management companies. Some PE firms approach these with the same logic, assuming it's also sticky because people don't easily switch property managers. But my experience shows property managers get replaced every three to five years because most people are dissatisfied with their property managers and constantly seek new bids.

Suddenly you have price competition and service level issues across the market. Your portfolio companies face distribution and go-to-market problems in an incredibly fragmented market with no clear decision-maker. Decisions often rest with homeowner associations and similar diffuse entities.

This distribution factor becomes crucial when I evaluate roll-up opportunities. In markets with stable, loyal customers, you have it easier. In fragmented markets with high customer churn, you're constantly fighting to prevent customers from leaving.

This is where I observe many roll-up strategies break down. The energy required to turn around multiple struggling businesses - or customers leaving after a few years ! - simultaneously often exceeds the synergies you can reasonably capture.

Strategic Clusters for Construction Investment Success

Now let’s apply these lessons to construction. Imagine you're a fund manager who just raised 10 billion euros for buy-and-build strategies, specifically targeting the entire construction value chain from upstream material production to downstream small general contractors in renovation.

You might want to focus on three strategic clusters.

First, material distribution and dealer networks. The logic here mirrors what Brad Jacobs does through logistics at QXO, but you might also approach it through last-mile distribution of construction materials. You target regionally dominant distributors of construction materials, especially for renovation, expansion, and civil engineering. These companies have their own warehousing, local fleets, and stable customer bases among craftsmen and small general contractors.

High repeat purchases for renovation, repair, and infrastructure maintenance. Established logistics systems. Technically simple operations with high cash conversion. I focus on DACH markets with highly fragmented markets and many family businesses, plus growth regions like the US Southeast.

Second, specialized trades with extreme customer binding. You might target HVAC, electrical, water installations, glass and window installation (but B2B !!!). These segments offer recurring revenue through maintenance and service contracts. Skilled labor shortages create pricing power. Strong local brand loyalty exists, and low price transparency creates competitive moats.

From what I observe, value creation in specialized trades comes through centralized service networks where you combine regional service teams to create cross-regional networks. You optimize personnel deployment and response times. Centralized training and HR become force multipliers, creating academies for skilled workers to better manage labor shortages while maintaining consistent quality standards.

Which leads to point 3, specialized civil engineering and infrastructure services. I target companies operating municipal infrastructure for wastewater, water, and cable trenches. Excavation companies, horizontal drilling technology, milling, and paving operations. These have high capital expenditure barriers and low margins, but incredibly sticky customers in municipalities and utilities.

For infrastructure services, the absolute key is a long-term framework contracts with municipalities that provide stable orders and better planning visibility. The reason why this might be a roll-up case for you is that the personnel needed is so specialized that it’s rare - and by buying these together, you can redeploy experts across a country to many more long-term contracts than the local players ever could.

But none of these would tickle my fancy enough.

What I find most interesting as an emerging opportunity to dive deeper into (not yet invest - I need to do more work !) is consolidating small and underutilized construction material manufacturers with high energy costs. You help with energy procurement and process energy transformation, providing capital for these improvements. I'm thinking about mid-sized brick and cement producers in Germany, Austria, or Northern Italy who still have relatively energy-intensive production processes. Their utilization went down the last 20 years, and their energy cost went up.

Insulation material producers in Northern Europe face the challenge of making their production more energy-efficient. Same case here (and in fact large insulation OEMs are doing exactly this, so not a secret). From what I see in Scandinavian and Benelux countries, there are many manufacturers who could benefit from this consolidation approach.

These companies could benefit significantly from joint energy purchasing or investments in more efficient energy technologies.

The Anti-Hero Reality Check In Construction Roll-ups

What would you avoid with your 10B fund? General contractors in building construction due to cyclical nature and high project dependency, when they don’t have anything of a recurring and predictable nature.

Architectural and planning offices because operational scaling is extremely tied to low-recurring project work.

Residential development is too speculative and again, too low-recurring project work, for buy-and-build strategies.

Which is also why you would also absolutely avoid any B2C-facing roll-ups - except when you would find an amazing subscription/maintenance logic, as in US-based pool servicing or home security.

Do you see the pattern?

Corporate actors, including private equity firms, engage in these types of acquisitions across a wide array of markets and industries, but regulators are increasingly scrutinizing these strategies. "Firms can use serial acquisitions to roll up markets, consolidate power, and undermine fair competition, all while jacking up prices and degrading quality," said Chair Lina M. Khan.

The construction sector offers genuine roll-up opportunities, but only if you understand where the real value levers exist. What I've convinced myself of is that you need businesses with predictable cashflows - a result of cash flow positive, high recurringness, sticky customers, and the opposite of low-frequency project work -, limited competition, and ideally immense brand/pricing power. Most importantly, you need to understand whether you're solving a real distribution problem or just creating complexity. And avoid most contractor-related businesses unless driven by sticky and hugely profitable maintenance contracts.

The question isn't whether construction can be consolidated. The question is whether you're building a machine that creates sustainable value or just burning capital in a fragmented market. From my observation, the difference between these outcomes lies entirely in which archetype you choose to follow.

Companies Mentioned

Berkshire Hathaway: https://www.berkshirehathaway.com/

Constellation Software: https://www.csisoftware.com/

QXO: https://www.qxo.com/

Thrasio: https://thrasio.com/

Follow the AEC_VC

Patric Hellermann: https://www.linkedin.com/in/aecvc/

Foundamental: https://www.foundamental.com/

#RollUps #PrivateEquity #ConstructionTech #BuyAndBuild #ValueCreation #AEC #Construction