.png)

In 2023, Shub and I published a thesis: between 2025 and 2027, AEC firms would be forced to rethink their entire software stack. We're now in 2026 and from what we're observing, that window seems to be open. Enterprise deals are closing in days, not quarters. Acquisitions are being justified on existential rather than financial grounds. And the companies at the intersection of geometry authoring and data infrastructure are shaping up to be among the most strategically valuable assets in AEC tech.

This Week On Practical Nerds - tl;dr

Enterprise CAD and data infrastructure deals are closing in days, not quarters, currently

The Consigli acquisition looks like a product and team bet

Brain plus heart equals the foundation for a $100B CAD business

Autodesk's pricing shift is forcing an IT stack reckoning across AEC

The first company to consolidate authoring and data infra will become the platform

🎧 Listen To This Practical Nerds Episode

Enterprise CAD and data infrastructure deals are closing in days, not quarters, currently

What suddenly switched on the enterprise customer side?

Two years ago, a $300K ACV deal in AEC took months of convincing, endless pilots, and a lot of patience. Today, Shub and I are watching deals in that range close in under two weeks. In one case from our portfolio that Shub flagged, the whole process - first conversation to signed contract - took less than two weeks. For anyone who has spent time trying to sell into large AEC firms, that is not normal. So what, in our view, has changed?

The way we see it, the answer has two parts - and both had to be true at the same time for this shift to happen.

Part one: years of product depth finally paying off

The first part is product readiness. Companies like Snaptrude, Speckle, Rayon, and CalcTree have been building for years. Shub has been following Snaptrude since 2017 or 2018, years before we eventually invested. And the thing about geometry - once you touch CAD, once you touch authoring, once you touch the data infrastructure of 3D design - you simply cannot shortcut it. You cannot vibe-code your way to enterprise-grade geometry tooling.

This is a point worth sitting with for a moment, because in an age where AI can generate functional software in hours, it is tempting to assume that speed of product development is now uniform across categories. It is not. The moment you touch geometric data - the moment your product needs to represent, manipulate, or store three-dimensional relationships between building elements - you are in a different league of technical complexity. You are dealing with precision requirements that have zero tolerance for error. You are dealing with file formats that carry decades of legacy decisions baked into them. You are dealing with interoperability constraints across a fragmented ecosystem of tools that architects, engineers, and contractors each use differently. Getting that right, at enterprise fidelity, takes years of iteration. There is no shortcut.

The reference cases make this concrete. Onshape raised over $100M and took roughly five years before it was genuinely enterprise-ready. Figma didn't cross a million in ARR for years. Revit - before it was Revit, when it was still being built by Charles River Software - took years to develop before Autodesk acquired it. Even with all the resources Autodesk brought to bear after that acquisition, it took more time before it became the dominant standard. This is just the nature of this space.

What Shub and I believe we're now seeing - for the first time across multiple companies simultaneously - is that several of these new-generation players crossed that enterprise readiness threshold in 2025. Not because they found a shortcut. Because they put in the years.

Part two: the pricing bomb that was always going to go off

The second part is customer readiness. And in our observation, this is actually the bigger and more structurally interesting shift. Something has materially changed on the buyer side - and it did not happen by accident.

I published a thesis in May 2023 where I argued that architecture firms and general contractors would be reevaluating their entire IT stack between 2025 and 2027. The reasoning was not speculative. It was rooted in a specific, observable dynamic: the teaser rates that Autodesk had offered large enterprise customers - discounted pricing structures designed to lock in volume commitments - were set to expire in that window. And simultaneously, Autodesk was already publicly on a path toward a consumption-based pricing model. More usage means more cost. For firms that are already operating on razor-thin margins, that is not a comfortable trajectory.

Large enterprise customers with large Autodesk contracts are not naive. They read the pricing roadmap. They attended the sales conversations. They understood what was coming. And crucially, they had a window of time to prepare - to evaluate alternatives, to run pilots, to build internal conviction around challenger tools before their existing contracts ran out. That preparation has been happening quietly for the last two to three years. What we are seeing now in deal velocity is the output of that preparation.

This, in our view, is not primarily an AI story. AI may be amplifying the pace of adoption once a decision is made - AI-native features in challenger tools make them more compelling, and the promise of AI applied to structured geometric data is genuinely exciting. But the underlying driver of the IT stack reevaluation is vendor lock-in economics, not AI. Architecture and construction firms were going to rethink their tooling stack regardless of whether ChatGPT existed. The pricing model shift would have forced it.

What AI has done, arguably, is compress the decision-making cycle on the customer side. Once a firm decides it wants to move, AI-native tools give it a forward-looking justification that makes the switch feel not just defensive - not just "we're moving away from Autodesk pricing risk" - but offensive. "We are moving toward a more intelligent, connected workflow." That reframe matters internally when you are trying to get sign-off from a CTO or a CFO.

We are now in 2026, sitting inside the 2025–2027 window. And the deal velocity we are seeing across our portfolio and beyond is, in our read, the direct and predictable consequence of forces that were set in motion years ago.

We think, the window of confluence between product readiness and customer adoption readiness has finally opened - and the companies that were already enterprise-ready are the ones capturing the moment.

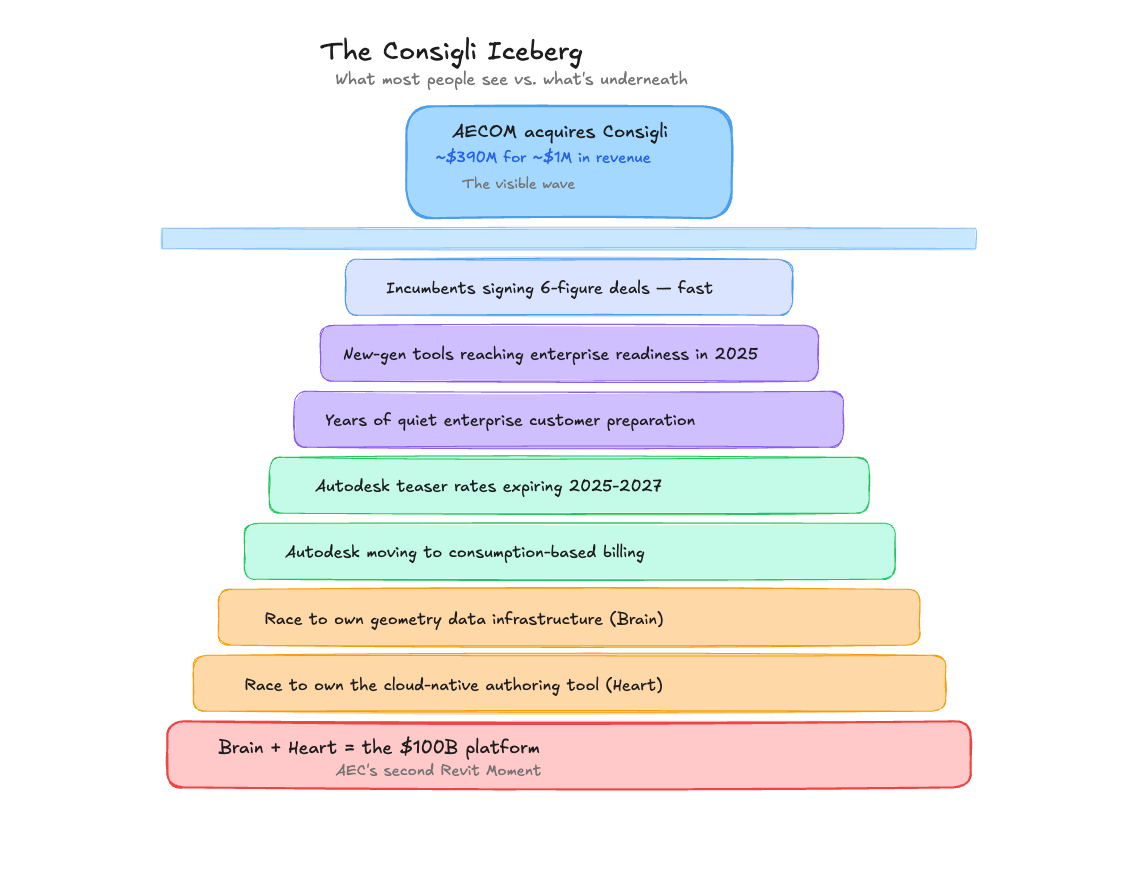

From the outside, the Consigli acquisition looks like a product and team bet

What does the Consigli deal actually tell us about strategic value in AEC?

AECOM acquired Consigli for approximately $390 million. That number surprised a lot of people - including other strategics who had been in conversations with Consigli at a meaningfully lower valuation not long before. The gap between what those earlier conversations implied and what AECOM ultimately paid is, in our view, one of the most instructive data points in recent AEC M&A history. So what is our read on what actually happened here?

The numbers tell a story - just not the one you'd expect

We dug into the publicly available financials. In Norway, every company is required to publish its accounts in the national corporate registry - so none of this is proprietary. Anyone with an LLM and five minutes can access it. What those numbers showed is that Consigli had roughly $1 million in fiscal year revenue in the year leading up to the acquisition. And that was down nearly 50% from the $2 million they had posted the year before.

Of that revenue, it looked to us like roughly half was subscription and half was services. That revenue composition matters. Services revenue in a software company is generally lower quality - it doesn't scale the same way, it ties up headcount, and it is harder to grow without linear cost increases. So you have a company with shrinking total revenue, a mixed revenue quality profile, and - as is typical for high-growth startups - a burning cost base. By any conventional financial analysis, there is no path from those numbers to a $390 million acquisition price.

No revenue multiple gets you there. No DCF built on those financials gets you there. No comparable transaction in the AEC software space, when you look at the underlying metrics, justifies that number on a pure financial basis.

And yet AECOM paid it. Which tells you the valuation was not built on financials.

What AECOM was actually buying

Our best read: this was a product acquisition and a team acquisition. AECOM looked at what Consigli had built - the depth of the technology, the architectural decisions behind the product, the caliber of the engineering team - and concluded two things. One, they could not build this themselves at the speed and fidelity required to remain competitive. Two, if a competitor acquired it instead, the consequences could be existential.

That second point is the one that strikes Shub and me as the most significant. From what we gathered about how the deal was rationalized internally at AECOM, the framing was stark: without this acquisition, the technology represented an existential threat to their business model. That is an extraordinary thing for a company of AECOM's stature to say publicly. AECOM operates at a scale that most AEC firms can only observe from a distance. When they use the word existential, they are not being dramatic for effect. They are describing a genuine strategic vulnerability.

The parallel to Revit is instructive here. When Autodesk acquired Revit - then still operating as Charles River Software - the company was not a revenue powerhouse. The technology was compelling but the commercial traction was modest. Autodesk had the strategic foresight to see that owning the authoring tool at the center of the architecture workflow would compound into an enormous position over time. That bet has delivered generational returns. AECOM, in our reading, is attempting a version of that same forward-looking logic now.

The ripple effect we're already watching

What's also interesting is what has happened in the market since the announcement. Shub and I have been tracking a pattern where large incumbents - not just AECOM, but other prominent firms across the architecture, engineering, and construction space - are quickly signing six-figure deals with companies across this new-generation tooling landscape. This is not limited to our portfolio. We are seeing it with firms from different geographies that we're in dialogue with.

It is tempting to attribute this to the Consigli acquisition acting as a trigger - a wake-up call moment that pushed hesitant incumbents into action. There is probably some truth to that. But Shub's read, which we find more plausible, is that the acquisition is more symptom than cause. The underlying currents - the pricing pressure, the product readiness, the accumulated internal pilots - were already in motion. Consigli is, in this framing, the first visible wave from a much larger offshore movement. There is more coming.

When a firm of AECOM's scale publicly frames a startup acquisition in existential terms, our read is that the competitive logic of the entire industry is shifting - and that the strategic premium attached to the right technology assets in AEC is only going to grow.

Brain plus heart equals the foundation for a $100B CAD business.

What does the company that wins AEC's design stack actually need to own?

If someone is going to build a $100 billion business in CAD - and Shub and I believe someone will - our conviction is that there are two assets they need to control. We think of them as the brain and the heart. And we think the companies that get closest to owning both will be valued not on what they earn today, but on what they make possible for the entire industry.

The brain: geometry data infrastructure

The brain is the data infrastructure of geometry. The ontology. The system that holds, structures, and connects all geometric data across a project lifecycle - from early feasibility sketches through detailed engineering models through construction coordination through facilities management. The thing that makes building information machine-readable, interoperable, and connectable to every other tool in the stack.

I've been calling this the bathtub. The image is intentional. A bathtub holds water. It doesn't care what kind of water you put in it. It doesn't prescribe the shape of what it contains. It just holds it, reliably, without leaking, in a way that lets you interact with it. That is what the geometry data infrastructure layer needs to do for building data. It needs to be the neutral, reliable, structured container that every other tool - every analysis application, every cost estimation engine, every AI feature, every downstream workflow - can trust and connect to.

The reason this doesn't exist today in a fully realized form is that the dominant incumbent, Autodesk, was never fully incentivized to build it. Revit's data model was designed in an era before cloud, before API-first thinking, before the expectation that everything would need to talk to everything else. It carries significant legacy constraints. The proprietary file formats that define so much of the AEC industry - .rvt, .dwg - are not built for the kind of open, connectable data infrastructure that the next generation of tooling requires. They were built for an era of desktop software and closed ecosystems. That served Autodesk's commercial interests at the time. It now serves as one of the primary pain points driving the migration we are observing.

A true geometry data infrastructure layer would be open enough to ingest data from any authoring tool, structured enough to make that data semantically meaningful, and flexible enough to accommodate the enormous variability in how different project types - a hospital, a bridge, a data center, a residential tower - actually organize and use geometric information. Building that is a multi-year technical challenge. The companies that are getting close to it are, in our view, among the most valuable assets in the entire AEC technology landscape.

The heart: the authoring tool

The heart is the authoring tool. The place where geometry is actually created and manipulated. Where architects spend their mornings designing facades. Where structural engineers iterate on load-bearing systems. Where MEP coordinators resolve clashes. Where contractors model constructability constraints. This is the tool that sits at the center of the highest-value, most cognitively demanding work in the built environment industry.

The authoring tool that wins the next generation, in our view, needs to satisfy a set of requirements that Revit structurally cannot meet. It needs to be browser-native - not because browser-native is aesthetically appealing, but because it removes the installation, versioning, and IT management overhead that creates friction in enterprise adoption. It needs to be multiplayer and concurrent - not in the approximate, file-sharing sense that BIM 360 approximates collaboration, but in the true sense that multiple people can work on the same model simultaneously without conflict resolution nightmares. And it needs to be genuinely generalist - covering the full project lifecycle from concept through construction, not just excelling in one phase and degrading in others.

That last requirement is harder than it sounds. There are tools in the market that do early-stage design very well but lose fidelity as projects move toward detailed engineering. There are tools that handle coordination well but are too technically demanding for conceptual work. The authoring tool that wins needs to hold its quality across the entire arc of a project. That breadth of capability is, in our observation, one of the key differentiators between the companies that are signing large enterprise deals today and those that are still stuck in the SMB and academia tier.

Why brain plus heart creates a platform, not just a product

The reason we keep coming back to this brain-plus-heart framing is that it describes something qualitatively different from a point solution. A company that owns both the geometry data infrastructure and the primary authoring tool does not just have two products. It has a platform. Everything else in the AEC technology stack - cost estimation, structural analysis, energy modeling, scheduling, procurement, facilities management - needs to either connect to that platform or become irrelevant.

This is the dynamic that made Autodesk so powerful for so long. Revit was not just an authoring tool. It became the de facto system of record for building geometry, which meant that every other software vendor in AEC had to either integrate with it or lose access to the most important data in the design process. Autodesk captured enormous value from that position - not just through Revit licensing, but through the entire ecosystem of products it could build on top of that data.

The next version of that platform will be built differently. It will be cloud-native. It will be API-first. It will have a data model that is structured for AI to actually use - not just AI that summarizes documents or generates images, but AI that can reason about geometric relationships, flag coordination issues, optimize structural systems, or generate compliant building configurations from a set of constraints. That is the long-term promise that, in our view, makes the brain-plus-heart combination so valuable.

Shub drew a comparison to how Microsoft and Alphabet evolved that resonates with us. Both built their dominance by owning the platform layer - the infrastructure that everything else in their respective ecosystems runs on top of. Windows and Office meant that every enterprise workflow ran through Microsoft's stack. Google Search and Android meant that every mobile and web interaction generated data for Alphabet's stack. In AEC, our belief is that the equivalent platform layer is geometric data infrastructure and the authoring tool that feeds it. Whoever controls both controls where the data lives - and therefore controls the leverage point for everything built on top.

We know which companies we think are in contention for these two roles. We won't name them here. But we've bet significant capital on the thesis that both will coexist for a meaningful period - each building depth in their respective lane, each accumulating a user base and a data asset that makes them strategically valuable. And then, at some point, the consolidation logic will become too compelling to resist.

Our instinct is that the trigger will be the first company in this space to raise $100 million or more. That capital, in the right hands, becomes the consolidation currency. A data infrastructure company with $100M in the bank looks at the best authoring tool and asks: what would it cost us not to own this? An authoring tool company with $100M looks at the best data infrastructure company and asks the same question. The answer, we suspect, will make the math look obvious in retrospect.

And when that consolidation happens, those companies will not be valued on trailing revenue. They will be valued on strategic position, on moat depth, and on the forward promise of sitting at the center of every design decision made on every project in the world. We would strongly caution any founder building in this space against exiting too early or at a price anchored purely to current year metrics. The strategic value of what the best companies here have built is, in our conviction, only beginning to be understood by the market.

The company that owns both the geometry data infrastructure and the authoring tool will, in our view, have the technical foundation to become the platform for a trillion-dollar industry - and the window to build that position is open right now.

A Confluence Framework

The AEC design stack is being rebuilt right now. Here is one way (among others) how Shub and I would frame key moves to watch and act on:

Recognize the pricing window for what it is. The IT stack reevaluation happening across AEC is not AI-driven hype. In our reading, it is a direct consequence of Autodesk's pricing model transition and expiring teaser contracts. This window runs through 2027. Companies that are enterprise-ready today are capturing outsized deals because the customer urgency is real and structurally driven.

Don't read the Consigli acquisition as a revenue story. It appears more as a product and team acquisition made under a self-perceived existential strategic pressure. M&A activity in this space should also be evaluated through the lens of strategic positioning, not only (trailing) revenue multiples. The gap between what a solution is worth to a motivated strategic acquirer versus a financial buyer is, in our observation, enormous - and that gap is only widening right now.

Think in terms of brain plus heart. Our conviction is that the winning architecture for the next-generation CAD platform requires both a generalist data infrastructure layer and a generalist authoring tool - browser-native, multiplayer, and built for the full project lifecycle. The first company to consolidate both assets at scale becomes the platform everything else is built on. Point solutions, however well-executed, will eventually need to orient around it.

Watch the snowball. The Consigli deal, in our view, is a symptom of deeper currents already in motion. Enterprise signings across the space are accelerating. Founders building in this space with real product depth and enterprise readiness should hold their nerve on valuation - the strategic value of what they've built is only beginning to be understood.

You Can Find More Analysis On The Practical Nerds Podcast

Spotify: https://open.spotify.com/show/1Q86tEwusNGwAmRdDqjFL4

Apple: https://podcasts.apple.com/de/podcast/practical-nerds/id1689880222

Foundamental: https://www.foundamental.com/

Subscribe to the Newsletter: https://www.linkedin.com/newsletters/practical-nerds-7180899738613882881/

Companies Mentioned

Revit: https://www.autodesk.com/products/revit

Snaptrude: https://www.snaptrude.com

Speckle: https://speckle.systems

Rayon: https://www.rayon.design

CalcTree: https://www.calctree.com

Enscape: https://enscape3d.com

Onshape: https://www.onshape.com

AECOM: https://www.aecom.com

Follow The Practical Nerds

Patric Hellermann: https://www.linkedin.com/in/aecvc/

Shub Bhattacharya: https://www.linkedin.com/in/shubhankar-bhattacharya-a1063a3/

Related Perspectives