Here we are for part 3 of the series.

Today, we go back to the 19th-century steelmaking industry.

The history of industrial capitalism is often misremembered as a linear narrative of invention leading directly to wealth, but this isn't necessarily the truth.

As we'll see, an analysis of the 19th-century steel revolution, in fact, reveals a more complex reality: invention is merely a precursor to value capture, and the mechanisms for capturing that value often require a fundamental restructuring of the business model itself.

Hence, in this article, I'm set to examine the economic architectures of the steel industry's transition from 1855 to 1901, juxtaposing the trials of Sir Henry Bessemer and the triumphs of Andrew Carnegie against the contemporary parallels of the project economy.

Let's dive in!

From luxury metal to industrial backbone: some history

Let's start with some history.

To fully appreciate the magnitude of the shift orchestrated by Bessemer and capitalized upon by Carnegie, we must first establish the economic and technical baseline of the mid-19th century.

In 1855, steel was an exotic luxury metal: expensive, slow to produce, and available only in small batches. Before Henry Bessemer's breakthrough, the dominant methods (blister steel cementation and Huntsman's crucible process) yielded mere tens of thousands of tons of steel per year. Crucible steelmaking was painstaking: craftsmen heated tiny clay pots of iron for hours to absorb carbon, producing only a few dozen pounds at a time: the result was superb but prohibitively costly (on the order of £40-60 per ton in the 1850s, or £7.2k pounds today at the lower end -> $9.8k per ton in today's dollars), at a time when wrought iron cost far less. It took at least a full day of laborious heating, stirring, and re-heating to refine a batch of steel from pig iron.

Bessemer's invention changed everything. In a dramatic 1856 demonstration, he showed that blasting air through molten pig iron could oxidize impurities and decarburize the iron in minutes, without any fuel beyond the initial melt. His pivoting, pear-shaped converter could turn 5 tons of pig iron into steel in 20-30 minutes, where the old methods required a day or more. The impact on cost was staggering: the Bessemer process slashed steel's price almost ten-fold, from roughly £40 per ton to about £6-7. By the 1870s, steel rails made with Bessemer's method were undercutting iron rails by such a margin that one British firm bragged it could undersell rivals by £10-15 per ton. In short, Bessemer discovered how to make steel 100x faster and at a tiny fraction of the cost, opening the door to an era where steel could go from a precious rarity to an everyday structural material.

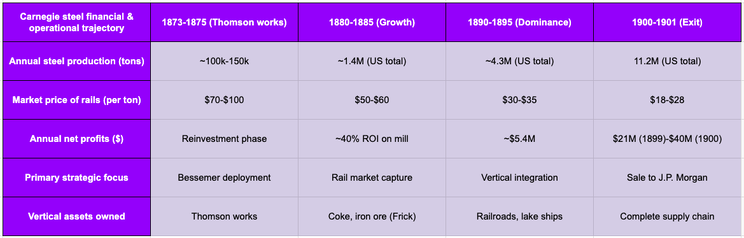

With cheap steel suddenly on offer, a massive market opportunity opened. The 1860s-1880s saw an explosion of demand as steel began to replace iron and even wood in the backbone of modern infrastructure. Railroads, for instance, rapidly switched from brittle iron rails (prone to cracking after a few years) to tough steel rails that lasted 15-20 times longer under heavy loads. By 1879, two-thirds of all new rails laid in the U.S. were steel, and the price of rails had plummeted over 80% from the mid-1860s to 1884. Structural engineering was revolutionized: bridges that would have been built in cast iron (and sometimes catastrophically collapsed, like the Dee Bridge in 1847) could now be made in steel with far greater safety. The first steel bridge, St. Louis's Eads Bridge, opened in 1874, proving steel's suitability for spanning great distances. Even shipbuilding was transformed as navies launched steel-hulled warships in the late 1870s. The total addressable market for affordable steel was effectively the entire industrializing world. In 1860, the U.S. had produced a paltry 13 thousand tons of steel but by 1880, output exceeded 1.4 million tons, and by 1900 the U.S. alone could smelt 11 million tons per year. What had been a niche material was becoming the foundation of modern economies.

Going back.

Bessemer now faced a fateful strategic choice: should he license his steelmaking patent to existing iron companies for a royalty, or should he build his own steel empire to exploit the process end-to-end? In the mid-19th century, the conventional wisdom for inventors was to patent and then monetize through licensing or sale of the rights, not to shoulder the enormous effort of manufacturing themselves. Thomas Edison, for example, made his early fortune by licensing or selling over 20 of his inventions to third parties. Eli Whitney had tried a similar approach with the cotton gin decades earlier. The patent system of that era actively encouraged inventors to profit as "non-practicing" innovators: an inventor could let established industrialists handle production, while he collected checks. Bessemer initially followed this path. Within two weeks of announcing his process in 1856, he had sold his first license. He granted licenses to a handful of ironmasters for lump sums and a per-ton royalty, essentially attempting to franchise the technology. However, early results were disastrous. The licensees couldn't replicate Bessemer's lab success: their steel came out brittle "like gravel", failing miserably in forging. By 1858, Bessemer's reputation was in tatters and his licensees demanded refunds, forcing him to buy back the licenses at a loss. This setback pushed Bessemer to consider the alternative: if no one else could make good steel from his process, he might have to do it himself. In a bold pivot, he built a steel plant in Sheffield in 1858 and partnered with experienced steel men to troubleshoot the process. Over the next few years, Bessemer and his partners solved the chemistry (with crucial help from Robert Mushet's manganese addition to fix brittleness) and improved the equipment. By 1862, his mill was producing quality steel and turning a profit. Yet, even as he proved a capable operator on a modest scale, Bessemer ultimately chose not to become the "Carnegie" of his era. He resumed licensing once the process was perfected, opting to collect royalties from many mills rather than build a huge enterprise of his own. It was, at the time, a very reasonable decision. Bessemer was an inventor at heart with limited capital and no background managing massive industrial operations. He had already gotten the process to market by licensing in America and across Europe.

The choice before him was risky: undertake a vast vertical integration effort (mines, furnaces, rolling mills, distribution) at age 45 and potentially go bankrupt, or stick to what he knew best (technology licensing and modest manufacturing partnerships). Given the norms of the 1850s, few would have faulted Bessemer for choosing the safer path. After all, people expected the "manufacturing men" to make the money. In that moment, it was not at all obvious that Bessemer had set the stage for a titanic fortune.

The inventor's millions vs the operator's billions

To understand the scale of Bessemer's opportunity cost, we must first understand what he earned from his invention. Bessemer's patents (filed in 1855-1856 in Britain, with equivalents abroad) had a lifespan of about 14 years, expiring around 1870. In that window, Bessemer set up a licensing program that charged steelmakers a royalty per ton of steel produced by his method. By the late 1860s, as steel production took off, these royalties were pouring in. From 1866 to 1868, Bessemer earned on the order of £200k per year ($27m per year today) in royalties (at £2 per ton of steel ingots), which is an enormous sum! After 1868, with the patent expiry imminent, he voluntarily slashed the royalty to 2 shillings 6 pence per ton to encourage even wider adoption. When the dust settled, Sir Henry (he was knighted in 1879) had received a total of "about one million pounds sterling" ($150m today) in royalties for his steel process (contemporary sources also put his take at roughly 5 million). This windfall made Bessemer a very rich man by Victorian standards (comfortably in the top tier of industrial wealth in Britain, though not the richest).

However, to grasp what Bessemer left on the table, we must contrast his earnings with the riches generated by Andrew Carnegie, the entrepreneur who most aggressively capitalized on the Bessemer process. Carnegie was a young Scottish-American industrialist who, after seeing Bessemer's steel in 1872, went all-in on steelmaking. He opened the Edgar Thomson Works in 1875 (one of the first Bessemer steel mills in the U.S.) and from that point forward, the profits simply exploded. In the late 1870s, Carnegie Steel was already earning $1.5m ($37m today) per year in profit while driving U.S. steel prices sharply downward. By 1890, with multiple mills and full vertical integration, Carnegie's operations were reportedly clearing $4-5m in annual profit. And then came the truly gargantuan sums: after absorbing competitors and weathering the 1890s depression, Carnegie Steel's net profit hit $21 million in 1899 and astonishingly $40m in 1900 ($1.5Bn!!). Finally, in 1901, Carnegie agreed to sell his steel company to J.P. Morgan, who rolled it into U.S. Steel. The sale price for Carnegie Steel was about $480m (approximately $18Bn today), of which Andrew Carnegie personally received $226 million in cash and bonds. Carnegie's personal take ($8.7Bn in today's money) made him the richest man in the world at that time.

At first blush, the conclusion seems blindingly obvious: Henry Bessemer made a colossal mistake in terms of business strategy. Here was the man who unlocked the Steel Age, arguably the single most important industrial innovation of the 19th century, yet he captured only a tiny fraction of the wealth that innovation generated. The lion's share went to men like Carnegie (and other steel barons in Germany, the U.S., and Britain) who did not invent the process but who did build the companies that exploited it.

It's easy (perhaps too easy) to label Bessemer's choice to license as naive. Some historians and business analysts have indeed pointed to the Bessemer-Carnegie contrast as a cautionary tale: innovators beware, the value of a breakthrough can flow right past you to the operators. It certainly appeared that Bessemer, sitting in his observatory in London, had "left 99% of the value on the table". The surface-level lesson seems to be that he should have done what Carnegie did (build a vertically integrated giant) and that failing to do so was a monumental opportunity lost.

Risk, capital, and the complexity of industrial operations

It's easy to pronounce Bessemer's licensing strategy a blunder with the benefit of hindsight. In reality, no one in 1855 knew that steel would become the literal pillar of the Industrial Revolution's next phase.

Bessemer was operating in a fog of uncertainty. In the mid-1850s, steel was still regarded as a finicky material; many experts doubted it could ever be made cheap enough to displace iron on a large scale. Recall that Bessemer's first attempt to commercialize his process ended in embarrassing failure: in those early years, there was a very real possibility that Bessemer's process might flop entirely due to unresolved technical issues. Moreover, alternative methods were nipping at Bessemer's heels. William Kelly in the U.S. had a similar pneumatic process; the open-hearth furnace was being developed in the 1860s by Siemens and Martin as a more controlled (if slower) way to make steel. For all Bessemer knew, a better or non-infringing process could have overtaken his within a decade. Even the market demand for steel, which seems obvious in retrospect, was not guaranteed. In the 1850s, railroads were well-served by iron rails (albeit less durable), and the great age of skyscrapers and steel warships was still decades away. There was no massive TAM, in modern founder's pitch deck terms.

Additionally, the risk profiles of the two paths (licensing vs. operating) were utterly different, and Bessemer's path had near-zero downside. By licensing his patents, Bessemer essentially locked in a guaranteed income stream so long as the industry adopted his process, while shielding himself from the hazards of day-to-day steel business. Once he set up his royalty agreements, economic swings were not his problem: if a mill produced steel, he got paid, boom or bust. Consider the volatile decades that followed: the steel industry went through gut-wrenching cycles, like the Panic of 1873, which triggered a four-year industrial depression; many iron and steel companies went under during that "Long Depression". Indeed, Carnegie built his first steel plant right as the 1873 crash hit, and he risked everything, borrowing heavily to complete the project amid the downturn. Had the recession lasted longer or demand not recovered, Carnegie could easily have been wiped out in the 1870s. Bessemer, by contrast, sailed through the 1870s unscathed: his royalty was a slice of whatever output occurred, and if output temporarily stalled, he had no payroll or debts to cover. Fast forward to the 1890s: another brutal depression in 1893 bankrupted a slew of U.S. steelmakers and led to massive industry consolidation. Carnegie himself faced price wars and labor unrest that could have sunk his firm in the early 1890s. These were existential risks borne by the operators. Bessemer slept soundly in London: to him, the worst-case scenario was that all the steelmakers using his patents might fail, but even in that unlikely event, he'd merely stop earning new royalties, not go bankrupt. Carnegie's worst case was far worse: total bankruptcy, loss of his personal fortune (which was tied up in the business), and thousands of employees out of work.

Another key factor was capital. Building a steel empire required immense and continuous investment, which was something Bessemer either could not or would not commit. When Andrew Carnegie constructed the Edgar Thomson Works in the 1870s, the initial investment was about $100k (around 2.5m today; Carnegie noted a tidy 40% annual return on that sum early on). But that was just the beginning. Carnegie and his partners plowed nearly all profits back into expansion: acquiring rival mills, building new furnaces and open-hearth installations, and crucially, integrating upstream into iron ore mines and coal/coke fields. By the 1890s Carnegie controlled vast ore deposits in Minnesota and had his own fleet of Great Lakes steamers and a dedicated railroad hauling ore to Pittsburgh. Each piece of this vertical chain cost huge sums, since Carnegie was effectively investing in mining companies, shipping companies, railroads, and steel mills all at once. Hence, it's worth asking: could Henry Bessemer have raised or marshaled such capital? It seems unlikely.

Bessemer was wealthy by 1860s standards, but not remotely in the league needed to finance global steel operations. He might have convinced outside investors to back him, but then he'd risk losing control. Plus, Bessemer's temperament was that of an inventor-businessman, not a captain of industry commanding vast financial resources. Bessemer got rich without tying up his own funds in blast furnaces and rolling mills. Carnegie, in contrast, led a financially precarious life for decades. At several points, Carnegie had nearly all his wealth tied up in illiquid industrial assets that could have become nearly worthless if the market turned or if his technology became obsolete. Moreover, we must remember that even great technologies have finite windows: by 1900 the Bessemer process itself was already being eclipsed by open-hearth steelmaking (which Carnegie had to adopt in the 1880s at additional expense).

Finally, we must ask: even if he had tried, could Henry Bessemer have been Andrew Carnegie? The skills and strategies that made Carnegie Steel triumphant went far beyond possession of the Bessemer patent. Carnegie was a master organizer and cost-cutter, drilled in railroad management techniques and ferociously focused on throughput and efficiency. He surrounded himself with brilliant operatives. He vertically integrated not just to own assets, but to optimize the entire value chain, squeezing out middleman profits and speeding up production from mine to finished rail. He leveraged close relationships with railroads (his biggest customers and also his former employers) to secure steady orders.

Henry Bessemer, on the other hand, was an engineer-inventor by training and inclination. He had no experience managing a large workforce or negotiating with coal suppliers or rail barons. His one attempt at operating a steel works in Sheffield was successful technically, but it was modest in scale and undertaken with partners who provided industry know-how. It is quite possible that if Bessemer had tried to scale up aggressively in the 1860s, he would have stumbled. Indeed, the history of invention is rife with brilliant inventors who were poor businessmen. Running a cutthroat commodities business in the Gilded Age required a different temperament and skillset than inventing a new process. Carnegie's success wasn't just due to Bessemer's process, but rather due to Carnegie's own innovations in management and integration: without those, merely having the patent might not have yielded such dominance.

Alright.

Now, it's time to take the learnings we've got so far and discuss how they are relevant to entrepreneurs in the project economy of the 21st century. Taking Bessemer and Carnegie's stories and re-adapting them to the contemporary era reveals, in my opinion, that entrepreneurs with valuable industrial technology today essentially find themselves in three distinct camps, each with profoundly different dynamics.

Let's discuss them one by one.

Camp 1: the better mousetrap

The first camp consists of entrepreneurs/companies developing (incrementally) superior versions of technologies that already exist (to some extent) and that customers already understand.

A few examples that come to mind here: improved battery energy storage systems that promise higher energy density or faster charging, thermal energy storage solutions with superior heat retention or lower cost per kilowatt-hour stored, carbon capture materials that pull CO2 from flue gas more efficiently, or modular construction systems that claim faster assembly times than competing prefab approaches.

These are substitute technologies, competing directly with established alternatives in categories where customers have existing procurement processes, performance benchmarks, and vendor relationships.

In my opinion, the uncomfortable truth about this position is that it represents perhaps the least compelling opportunity in modern industrial markets, despite often attracting a good chunk of attention and capital. Venture investors find substitute technologies intellectually seductive because the value proposition seems straightforward: if your battery stores twenty percent more energy than the incumbent solution, surely customers will pay a premium or you will capture market share. The way I see it here is that the fundamental problem is structural and unavoidable: when you offer an improved version of something customers (to some extent) already buy, you invite immediate replication and margin compression. Your innovation becomes a specification race where competitors match your improvements within product cycles, systematically eroding whatever pricing power you might have temporarily enjoyed. The market quickly commoditizes your advantage.

This is not a failure of execution or marketing, it is the inevitable consequence of competing in categories where the basis of competition is transparent and the barriers to replication are modest. Consider what happens in practice. Let's take the battery example. You develop a battery module with fifteen percent better energy density than the current market leader. You raise capital, perhaps build manufacturing capacity, and begin selling to customers. Initially, you might command a premium price because your specifications are superior. But your competitors are not standing still. They are working on their own improvements, and because battery chemistry and cell design are well-understood domains with established research pathways, they will close the gap. Within eighteen months, multiple vendors will offer comparable energy density. At that point, the basis of competition shifts entirely to price, and price competition in hardware manufacturing is a game won by whoever can achieve the lowest cost of production. This usually means whoever has the largest scale and the most favorable labor and material costs, which for most hardware categories means established players with massive factories in regions with structural cost advantages.

The dynamic plays out almost consistently across industrial hardware sectors. The lithium-ion battery market exemplifies the pattern perfectly. Dozens of well-funded companies have developed battery chemistries or form factors with genuinely superior performance characteristics: better energy density, longer cycle life, improved safety profiles, faster charging capabilities. Yet the overwhelming majority face punishing economics. Manufacturing has concentrated in China and other Asian markets where companies have invested billions in gigafactories and supply chain integration. These manufacturers can produce at costs that newer entrants simply cannot match, especially when many are willing to operate at or near breakeven to gain market share and capacity utilization. The result is that technical superiority becomes almost irrelevant to commercial outcomes. A battery that performs 20% better but costs 50% more to manufacture loses in the market to the adequate, cheap alternative (unless it's for very specific/dedicated usecases). Product differentiation evaporates faster than entrepreneurs expect, and margins compress toward commodity levels.

The solar panel manufacturing industry tells an even starker version of this story. Multiple waves of solar technology startups promised revolutionary improvements: higher conversion efficiency, novel materials, innovative manufacturing processes. Some genuinely achieved their technical goals. Yet, the top solar manufacturers collectively lost $4Bn in 2024 despite shipping record volumes. Why? Because solar panels became a commodity where the winning strategy was manufacturing at massive scale with ruthless cost discipline, not developing marginally better technology. The manufacturers with superior panels but higher costs lost market share to those with adequate panels at lower prices. Even companies with significant technical leads found themselves unable to defend pricing power as competitors closed performance gaps and Chinese manufacturers flooded the market with cheap capacity.

This is not to say that success is impossible in the "substitute technology" camp. NVIDIA demonstrates that even in a category as established as graphics processors, sustained technical leadership combined with ecosystem lock-in can create extraordinary value. But NVIDIA represents the exception that proves the rule, and understanding why NVIDIA succeeded where countless other "better-mousetrap" ventures failed reveals exactly what is required to win in this position. NVIDIA's defensibility came not primarily from having faster chips (though they did), but from building an entire software ecosystem around their hardware. CUDA, their parallel computing platform, created genuine switching costs. Developers learned CUDA, built applications on CUDA, optimized their workflows around CUDA. Moving to a competing chip architecture meant rewriting code, retraining teams, and potentially degrading performance. These switching costs compounded over time as the CUDA ecosystem deepened, creating a moat that technical specifications alone could never provide. The AI boom then amplified this advantage: when machine learning researchers standardized on NVIDIA GPUs for training models, it created network effects where the best tools, libraries, and talent all oriented around NVIDIA's platform. At that point, even if a competitor developed a chip with superior raw performance, customers faced prohibitive costs to switch their entire stack.

The lesson is that winning in the substitute technology camp requires far more than better specifications. You need either network effects, substantial switching costs, or manufacturing advantages that take competitors years to replicate. Most substitute technology ventures possess none of these structural advantages: they have a better component competing in a market where components are increasingly commoditized, and no amount of superior engineering can overcome the fundamental economics of that position.

The trap is particularly insidious because substitute technologies often start strong: the first customers might genuinely value your superior performance and pay a premium for it. This, however, creates false confidence: you see initial traction and assume you have found product-market fit. You raise growth capital to scale manufacturing and expand sales. But you might have confused early adopter enthusiasm with a defensible market position. As you scale, you discover that the bulk market is far more price-sensitive than early adopters, that competitors are rapidly closing performance gaps, and that your unit economics are underwater at competitive pricing. By the time this reality becomes clear, you have invested millions that will never generate adequate returns.

There is also a more subtle issue that makes the substitute camp challenging: you end up competing on dimensions that matter less and less to customers as markets mature. In early markets, performance is everything, but as technology matures, incremental improvements matter less vs. reliability, financing terms, operational simplicity, pricing.

As I made it clear enough, at least for me (personal view), this represents the least compelling camp. Obviously, this does not mean no one should pursue substitute technology ventures, but it does mean you should enter this camp with eyes wide open about the challenges and with a clear plan for building defensibility beyond technical performance.

Let's dive into the second possibility.

Camp 2: the novel tech (with vertical integration)

The second camp is fundamentally different and considerably more interesting, imo. Here, companies are developing genuinely novel technologies that customers do not yet understand and that require significant adaptation of workflows, processes, or operational assumptions. You are not offering a better version of something customers already buy, you are proposing an entirely new way of solving a problem or executing work. The technology creates value through disruption rather than substitution, and this distinction changes everything about the strategic landscape.

Let's speak in more practical terms.

The way I see it, construction robotics exemplifies this dynamic perfectly. When you introduce a bricklaying robot or an automated shingle installation system, you are not offering a better version of a tool that contractors already use. There is no equivalent/alternative to a robot that lays bricks 24/7 while a human mason adjusts each brick and manages mortar. You are proposing a fundamentally different way of executing work that has been done manually, with hand tools, for centuries. The contractor's entire job site workflow must adapt: the sequencing of trades, the layout of materials, the composition of crews, even the design of scaffolding and work platforms. Because your technology demands operational adaptation and because traditional players lack both the expertise and the incentive to deploy it properly, you cannot simply sell or license the technology and expect widespread adoption. The fundamental barrier is not skepticism about your technology's potential, it is something far more intractable: your customers cannot afford to bear any technology risk whatsoever.

Consider what this means in practice. A general contractor running a construction project operates on margins that might be three to five percent of the total contract value. Their project schedule is a delicate choreography of dozens of trades, each dependent on the others completing their work on time. Any delay cascades through the entire sequence, and delays cost real money (e.g. idle equipment, extended overhead, liquidated damages clauses, etc.). In this environment, a bricklaying robot that does not work perfectly is not very valuable: the failure rate means the robot will inevitably cause a delay at some point, and that delay will eat the contractor's entire margin on the project. Worse, it will damage relationships with the owner and create coordination problems with other trades who planned their work around the masonry being complete on schedule.

Hence, the contractor's calculus is brutally simple: manual construction with human masons might be slower and more expensive, but it is predictable. They know exactly how long it takes to lay a thousand bricks, they know how to handle weather delays and material issues, and they know their crews can adapt when problems arise. Your robot promises to be faster and cheaper, but it introduces uncertainty. What happens when it malfunctions on site? How long will repairs take? Can the crew continue working manually while waiting for a technician? What if the robot requires specific site conditions that conflict with other trades? Every one of these questions represents potential delay, and potential delay represents existential risk to the contractor's profit and reputation.

This risk aversion is not irrational or backwards-thinking. It is the rational response of businesses operating with thin margins in an industry where execution risk is high and schedules are unforgiving. The contractor cannot afford to be your beta tester. They cannot afford to debug your technology on a live project where dozens of other people are depending on them to deliver on time. Even if they intellectually believe your technology will eventually work perfectly, they cannot take the chance that "eventually" happens after they have missed deadlines and burned through their contingency budget.

The solution to this deployment challenge is vertical integration: you must control enough of the execution stack to ensure your technology is used properly and to capture the value it creates. This does not necessarily mean you must become a traditional general contractor doing every aspect of construction, but it does mean you need to own the outcome in a way that licensing or equipment sales never allows, e.g. positioning yourself as a specialized subcontractor who handles specific scopes of work using your robotic systems. This way, you control your crews, your processes, your quality standards, and you deliver finished work to general contractors or developers. In this model, the robot is your competitive advantage, not a product you are trying to sell. You bid on projects, execute them more efficiently than manual competitors thanks to your technology, and capture the margin between your lower costs and market pricing. Clearly, this model works only if the robotic solution you've developed executes jobs that are a clear line item in your (prospective) customer's P&L statement.

That said, I think this approach (vertical integration) can extend well beyond contech robotics to any genuinely novel industrial technology that requires ecosystem adaptation.

Let's suppose you've built a revolutionary approach to producing green steel in microfactories. This technology might work brilliantly, producing steel at costs competitive with traditional blast furnaces but with dramatically lower capital requirements and carbon emissions. The technology has been proven in pilot operations, and the unit economics are extremely attractive. The natural instinct might be to license this process to existing steelmakers or to sell the microfactory equipment to industrial customers who want captive steel production: but we've seen this story already, haven't we?

In my opinion, the winning move here is vertical integration: you must build your own steel production facilities, operate them yourself, and sell finished steel products to end customers. You become a steel company that happens to use revolutionary production technology, not a technology company trying to sell equipment to resistant incumbents. It's clear that this approach demands far more capital than equipment sales would require, and it means competing in the brutally competitive global steel market. By owning the production facilities, these companies can optimize the entire operation around their novel process, prove the economics at scale, and capture the full margin and value creation between their low production costs and market steel prices (for this to work, your unit economics must be significantly and not just marginally better than your competitors).

The vertical integration path is high-risk and high-reward, but for genuinely novel industrial technology that requires ecosystem adaptation, it is the best (and often the only) path to capturing significant value.

Camp 3: the system integrator

The third camp consists of companies that neither invent breakthrough technologies nor develop superior substitutes, but instead excel at taking proven components from the market and assembling them into complete solutions that customers will actually buy. More specifically, they take the components from Camp 1 companies and "servitize" their deployment to customers. The system integrator looks at the industrial landscape through an entirely different lens than the other two camps. I've talked extensively about this here, but allow me to share some details below.

Where the substitute technology camp sees specifications to improve and the novel technology camp sees new capabilities to commercialize, the system integrator sees deployment gaps to bridge. They observe that industrial markets are littered with perfectly functional technologies trapped in what we might call pilot purgatory: proven concepts that have not achieved widespread deployment because no one has figured out how to deliver them at scale with business models that customers understand and trust. These orphaned technologies represent enormous trapped value, and the integrator's innovation happens entirely at the packaging layer. They combine off-the-shelf hardware with software, wrap everything in as-a-service contracts that eliminate customer capital risk and operational complexity, and standardize deployment processes until what was once a bespoke engineering project becomes a repeatable product.

The renewable energy sector has demonstrated this model's power with devastating clarity. As we discussed earlier, solar panel manufacturers collectively lost billions while manufacturing record volumes, trapped in commoditized hardware markets with razor-thin margins. Meanwhile, NextEra Energy built a market capitalization exceeding $190Bn (at the time of writing) by being exceptionally good at deploying those same commoditized panels. NextEra invented nothing: they did not develop novel photovoltaic materials or revolutionary turbine designs; rather, their innovation was entirely in how they packaged and delivered renewable energy. They took proven hardware from struggling manufacturers and turned it into a highly profitable service offering by solving all the messy challenges between technology and customer adoption.

This arbitrage opportunity is structural and repeatable across industrial sectors. The pattern emerges wherever there is a gap between technical capability and market deployment: the manufacturers who develop the underlying technology are often technology-focused companies at their core, with leadership teams, organizational structures, and cultures built around engineering excellence and product development. They excel at making things work and improving performance specifications. However, what they consistently lack is expertise in project development, customer financing, risk management, and long-term operations, because these capabilities require entirely different organizational DNA. When a thermal energy storage manufacturer tries to transition from selling equipment to offering heat-as-a-service, they are attempting to transform their entire company into something fundamentally different. The cultural shift required is profound: from optimizing hardware specifications to optimizing financial structures, from managing manufacturing operations to managing multi-decade service contracts, from selling products to operating assets.

The system integrator's approach begins with what we might call mining the technology shelf. They systematically scan the landscape for proven technologies that are underdeployed relative to their potential, not because the technology is deficient but because it has not been packaged in a way that customers can easily consume. Consider industrial process heat, which accounts for roughly twenty percent of global energy use and emissions: multiple thermal energy storage manufacturers have developed functional systems using variations of resistive heating and high-capacity materials like refractory bricks or molten salt. The technology works, it has been demonstrated in multiple installations. Yet widespread adoption has remained elusive because manufacturers are selling equipment to industrial customers who do not want to become experts in thermal storage, who do not want to make multi-million dollar capital investments in unfamiliar technology, and who cannot easily navigate the complexity of grid interconnection and energy market participation. This is a textbook system integration opportunity.

The integrator's value creation happens at three distinct layers, each essential to transforming stranded technology into a deployable solution.

First is technical integration: making disparate components work together reliably. In the thermal energy storage example, this means integrating the storage hardware with grid interconnection equipment, control systems, monitoring software, and the customer's existing thermal processes. None of these components is particularly novel individually, but making them function as a reliable, optimized system requires deep expertise. The integrator develops this expertise across multiple deployments, learning which combinations work best, how to handle edge cases, and how to design for maintainability and long-term performance.

The second layer is business model innovation, which is often more important than technical integration. The industrial customers who need thermal storage or carbon capture or any other capital-intensive technology are not primarily constrained by the availability of hardware: they are constrained by capital allocation decisions, risk aversion, and organizational bandwidth. A cement plant operator has a finite capital budget that must cover maintenance of existing equipment, expansion of capacity, and regulatory compliance, so asking them to allocate millions of dollars to install a thermal storage system requires them to become experts in a technology outside their core competence, to underwrite the risk that it might not perform as promised, and to tie up capital that could be deployed elsewhere. These barriers are higher than any technical challenge. The system integrator dissolves these barriers by offering heat-as-a-service: they install the thermal storage system at their own expense (or more precisely, they structure project finance to fund the installation through specialized infrastructure investors). The customer signs a long-term contract to purchase heat at a predictable price, often structured to guarantee savings relative to their current energy costs: this way, the customer makes no capital investment, takes no technology risk, and receives guaranteed performance - if the system fails to deliver, the integrator absorbs the loss, not the customer.

This transformation from capital expenditure to operating expense is enormously powerful because it aligns the incentives perfectly. The integrator only makes money if the system performs as promised over the contract lifetime, so they have every incentive to design for reliability, to optimize operations, and to maintain the equipment properly. The customer gets a simple utility-like service with no operational complexity. The gap between these positions explains why as-a-service models have proliferated across industrial technology: they solve the adoption problem more effectively than any amount of technical improvement possibly could.

The third layer is operational excellence and continuous optimization. Once the integrator has deployed multiple systems, they begin to accumulate data and expertise that creates a genuine advantage.

Ulitmately, the system integrator model offers a fundamentally different risk-return profile than either of the other camps: they are not betting on scientific breakthroughs or unproven processes, but on their ability to execute deployment better than incumbents, which is a manageable and quantifiable risk. And by controlling the customer relationship and owning the deployment process through long-term service contracts, they capture far more value than technology licensors or equipment sellers ever achieve: they sit at the point where value is actually delivered to end customers, and they structure contracts that give them a share of that value over decades.

There are, however, critical success factors that determine whether a system integration approach will generate venture-scale returns or devolve into a sophisticated consulting business. I'll leave these to my previous article to not bore you will all the details here.

Alright. Time to bring this article home.

Conclusions

As we've seen, the story of Bessemer and Carnegie, refracted through today's industrial technology landscape, reveals a truth that cuts against the prevailing narrative: invention alone captures only a fraction of the value that execution ultimately delivers. Clearly, the lesson is more nuanced than simply declaring that operators always beat inventors: what matters is understanding which model fits the structural realities of your market at your specific moment in time.

Carnegie's ruthless vertical integration made perfect sense in the 1870s: steel demand was exploding, the technology was proven, and controlling the entire value chain created unassailable cost advantages. Bessemer's licensing strategy left the vast majority of value on the table because he positioned himself as a toll collector rather than as the operator generating real profits. The gap between Bessemer's $150 and Carnegie's nearly $9Bn (in today's terms) stands as perhaps the most dramatic illustration in industrial history of how execution economics dwarf invention economics when technologies mature and scale.

Yet, Carnegie's model is not a universal prescription for today's entrepreneurs.

Ultimately, the broader lesson is this: in project-based industries, value accrues to those who solve the last-mile problems between technology and customer adoption (or vertically integrate the technology themselves). The entrepreneurs who recognize this shift and position themselves accordingly are the ones who will build the next great fortunes while actually reshaping how we build our world.

If you're building in infrastructure or the project economy, reach out to us at Foundamental - we'd love to hear what you're working on!

More appetite for this type of content?

Subscribe to my newsletter for more "real-world" startups and industry insights - I post monthly!

Head to Foundamental's website, and check our "Perspectives" for more videos, podcasts, and articles on anything real-world and AEC.