The $15 Trillion Project Economy: Why Global Construction Has to Double by 2040

Global construction hit $15T but must double by 2040 to meet demand. Inside the data, the gap, and what it means for ConTech investors and builders.

The $15 Trillion Project Economy: Why Global Construction Has to Double by 2040

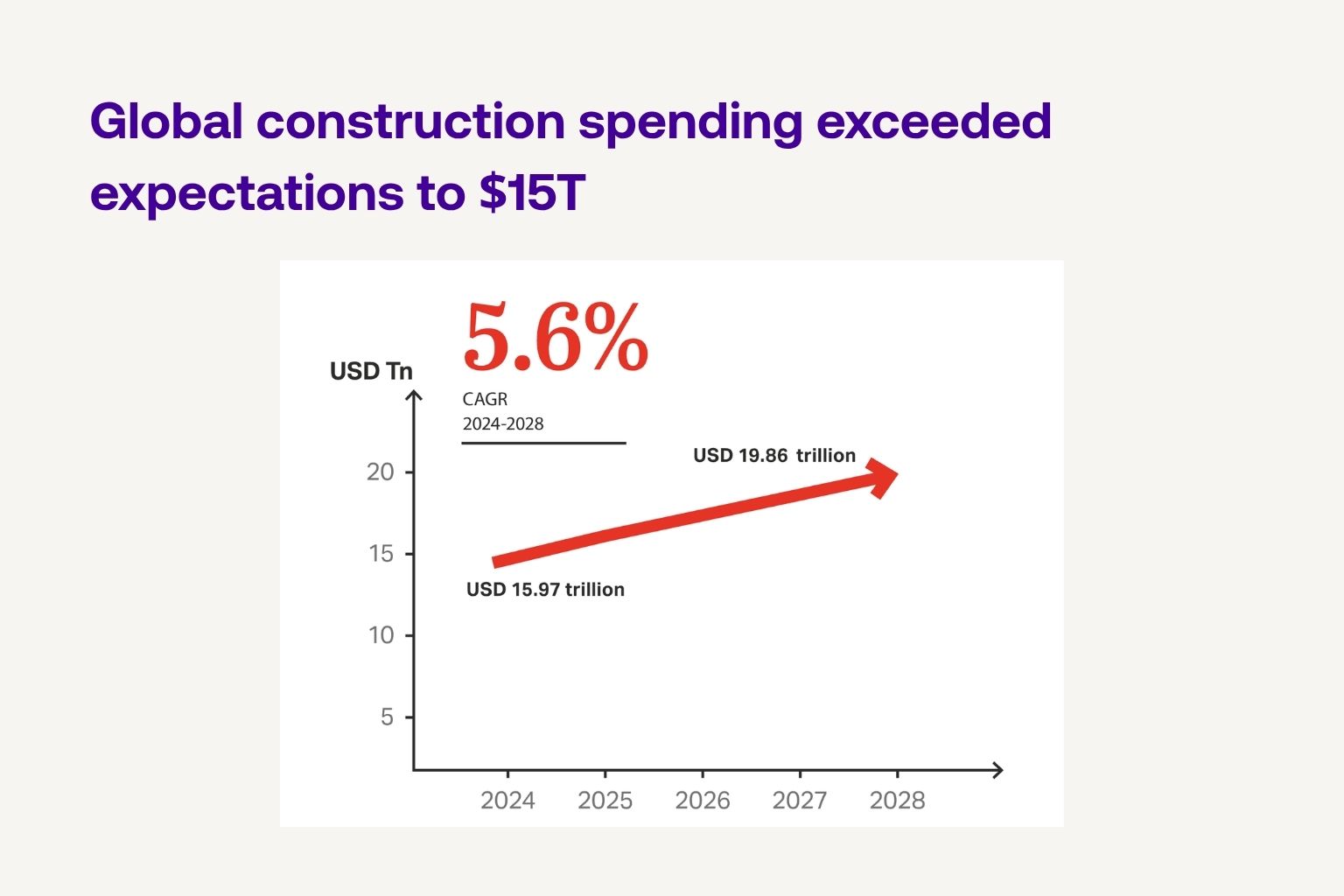

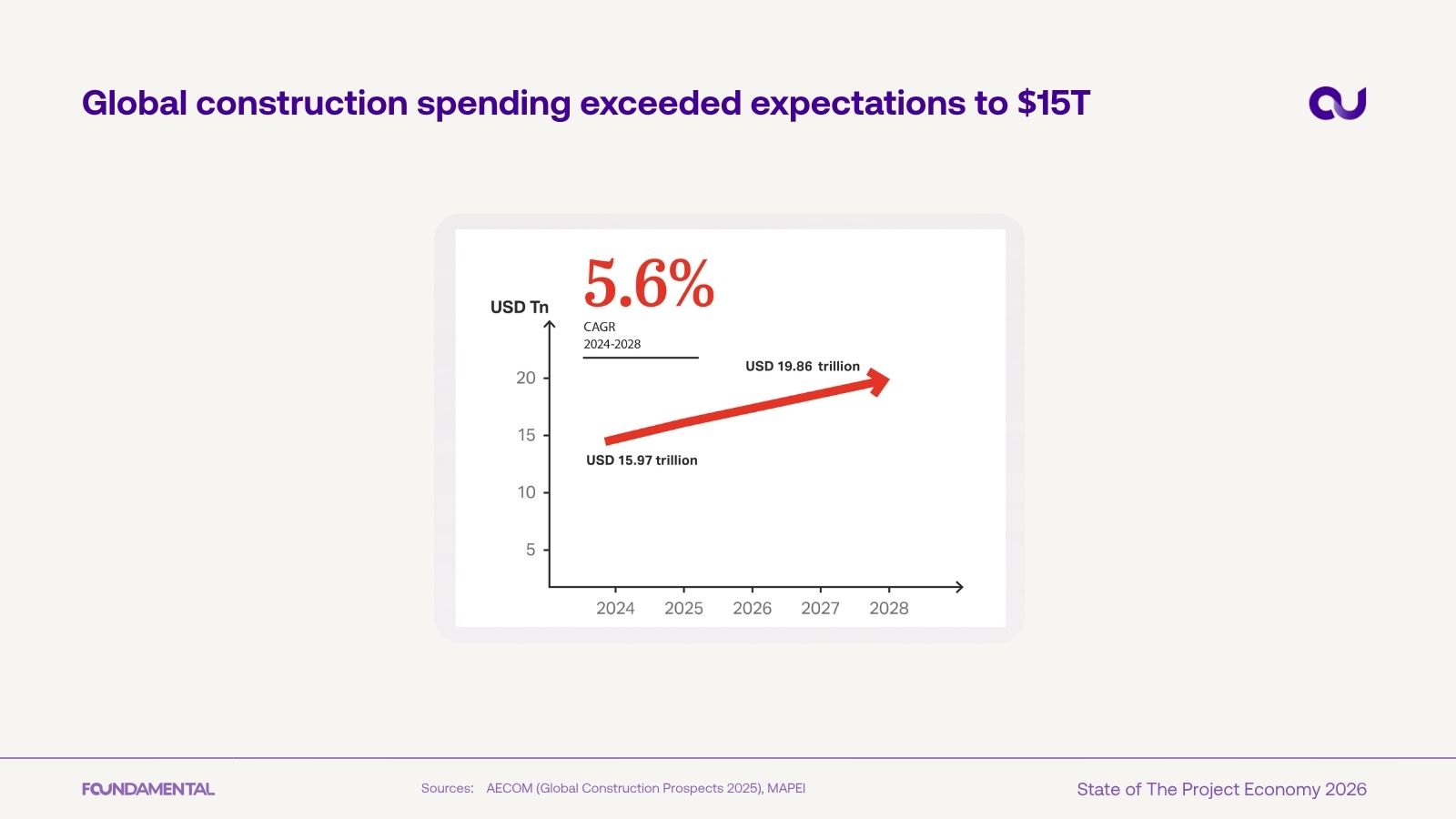

Global construction reached roughly $15 trillion in annual spending. That beat the forecasts. It also makes construction the single largest industry in the world by output.

Here's the harder number. To meet the demand expected by 2040, that output has to roughly double. Even the optimistic scenario falls about 20% short.

That gap, between what the world needs built and what it can actually build, is the project economy. This article covers what the term means, why the gap exists, where capital is concentrating, and what it means for you, whether you're building a company, investing in one, or running a construction business today.

What is the "project economy"?

The project economy is the full stack that turns investment into built physical capacity: capital, labor, materials, and technology. It covers the contractors and engineers who deliver projects, the materials and equipment that go into them, the financing that moves through them, and the technology layer that increasingly decides whether a project lands on time and on budget.

The term is deliberate. "Construction" makes people picture a job site. The project economy is broader. It's the semiconductor fab that has to be built before it makes a single chip. The data center that has to be powered and cooled before it trains a model. The grid that has to be upgraded before any of it runs. Seen this way, construction isn't a sector. It's the bottleneck layer for almost everything else that gets built.

A $15 trillion market that beat expectations

Construction spending exceeded expectations to reach about $15 trillion globally. It's a market that tracks economic output closely. Construction activity is highly correlated with GDP growth, which is part of why it's so large and so persistent.

Infrastructure leads every construction sub-sector, growing at a 5.1% CAGR between 2020 and 2025. And the pattern behind the headline is simple. The world is investing in physical capital at a scale it never has before. The Gross Fixed Capital Formation index has grown roughly 30 times since 1960. There has never been more money going into building things.

The 2040 demand gap

Now the problem. Construction is already one of the largest industries on earth, but its growth rate, excluding China, would need to double to meet 2040 demand. On the current trajectory, output falls short by around $40 trillion in cumulative terms by 2040. Even the more optimistic supply scenario still lands roughly 20% below what's needed.

This is the core of the thesis. The demand isn't in question. Governments, hyperscalers, and industrial players have committed the capital. What's in question is whether the industry can deliver against it. The constraint is buildability, not appetite.

.jpg)

Why the gap exists

Three forces sit underneath the gap. Productivity, which has barely moved in two decades. The workforce, which is projected to shrink across every major Western construction market through 2040. And cost, with materials and equipment prices climbing sharply since 2020. Together they explain why more money hasn't closed the gap, and why even the optimistic case still falls short. Each gets its own treatment later in this series.

Capital is concentrating, not spreading

More capital is flowing into physical assets than ever. But not evenly. Capital expenditure concentrates in five countries: China, Germany, France, India, and the United States. Those five take a disproportionate share of global fixed capital formation.

The concentration shows up in odd places. Iceland's construction index hit 313. In relative terms, small open economies are outbuilding the largest. The point is that the project economy isn't one global market moving in unison. It's a set of regional markets with very different growth rates, cost structures, and levels of technology adoption.

The growth has moved East

Look at where the growth is going and the center of gravity has shifted. China and India alone account for 40% of global construction growth between 2020 and 2030. China is 26.1% of that growth, India 14.1%, the United States 11.1%. The rest is spread thin.

The Western picture is more nuanced than a simple decline. Western contractors are still growing revenue. What they're losing is market cap. Investors are revaluing the traditional contractor model downward even as the businesses hold or grow their top line. The gap between revenue growth and valuation growth is one of the clearest signals in the data. It points to a market that no longer believes pure execution is where the value sits.

Where value is actually captured

That point reframes the whole opportunity. Since 2008, building-products companies have captured more than 9 points of return-on-invested-capital expansion. Over the same period, contractors and materials companies went nowhere.

The value in the project economy has accrued to products and IP, not to execution. Companies that own a differentiated product, process, or piece of technology have pulled away from companies that simply deliver the work. If you're deciding where to build or invest, this is the most important pattern in the market: the economics reward what you own, not how much you execute.

ConTech is stepping into the gap

The technology layer is responding. Construction-tech funding added roughly $3 billion in 2025, capital flowing in to help close the gap the demand numbers expose.

That funding isn't evenly distributed, and not every category has worked. Several of the most heavily funded approaches to lowering construction costs have stalled, which is a topic of its own. But the direction is clear. The same gap that makes the 2040 numbers look impossible is what makes the technology opportunity real. If the industry could already deliver against demand, there'd be nothing to build toward.

What this means for you

If you're a founder, the value-capture pattern is the one to internalize. The market rewards owning a product, a process, or infrastructure, not selling execution by the hour. The delivery gap is large enough to support real businesses, but the durable ones will look more like product companies than service companies.

If you're an investor, the signal is the divergence between revenue and valuation in the incumbent contractor base, set against the ROIC expansion in building products. Capital is already voting on where value sits. The open question is which parts of the technology layer can capture a share of the $40 trillion delivery gap rather than competing in the low-margin execution layer beneath it.

If you're a builder or operator, the demand is structural and it isn't going away. The constraint on your business over the next 15 years is far more likely to be delivery capacity, labor, and cost than a shortage of work. That turns technology adoption from a nice-to-have into the lever that decides whether you can capture demand that's already there.

The rest of this series breaks the project economy into its parts: the five demand drivers pulling capital into the market, the four bottlenecks keeping the industry from delivering, where capital is actually flowing, and the company archetypes built to close the gap.