“Everyone” in venture "knows" that the smart money is in software. Leaving aside that this, in itself, is debatable, does it really hold true specifically in AEC/the project economy?

Short answer: no.

As a matter of fact, the public markets have been calling horsesh*t on that for six years.

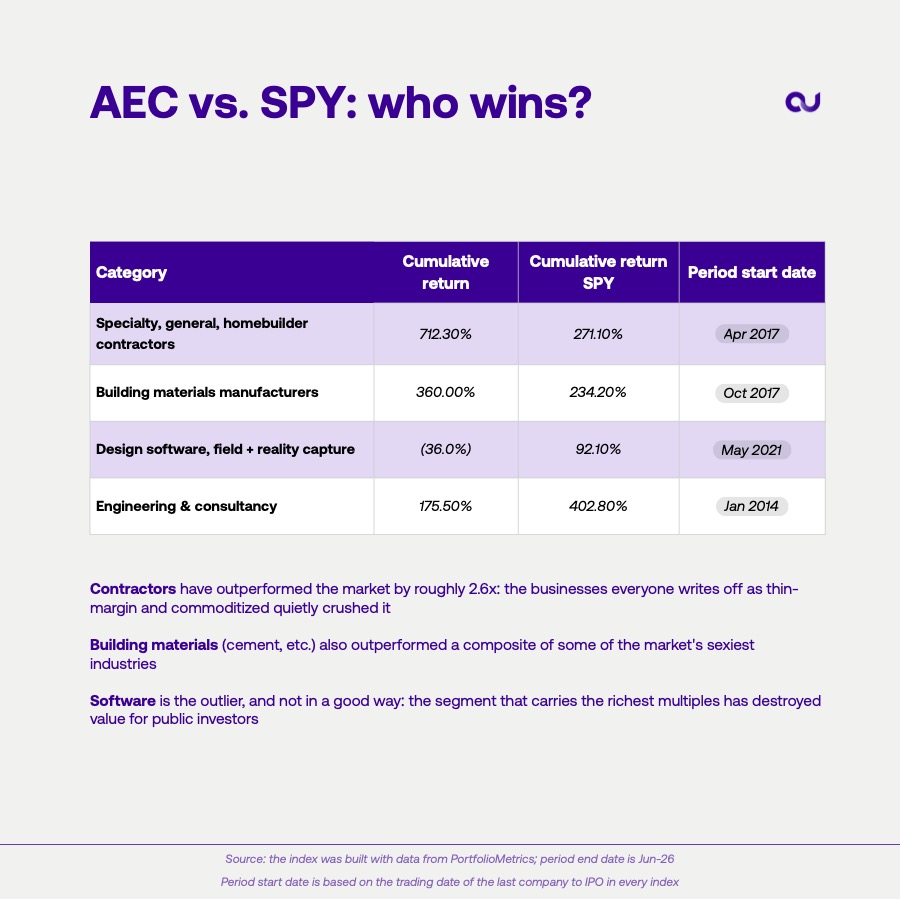

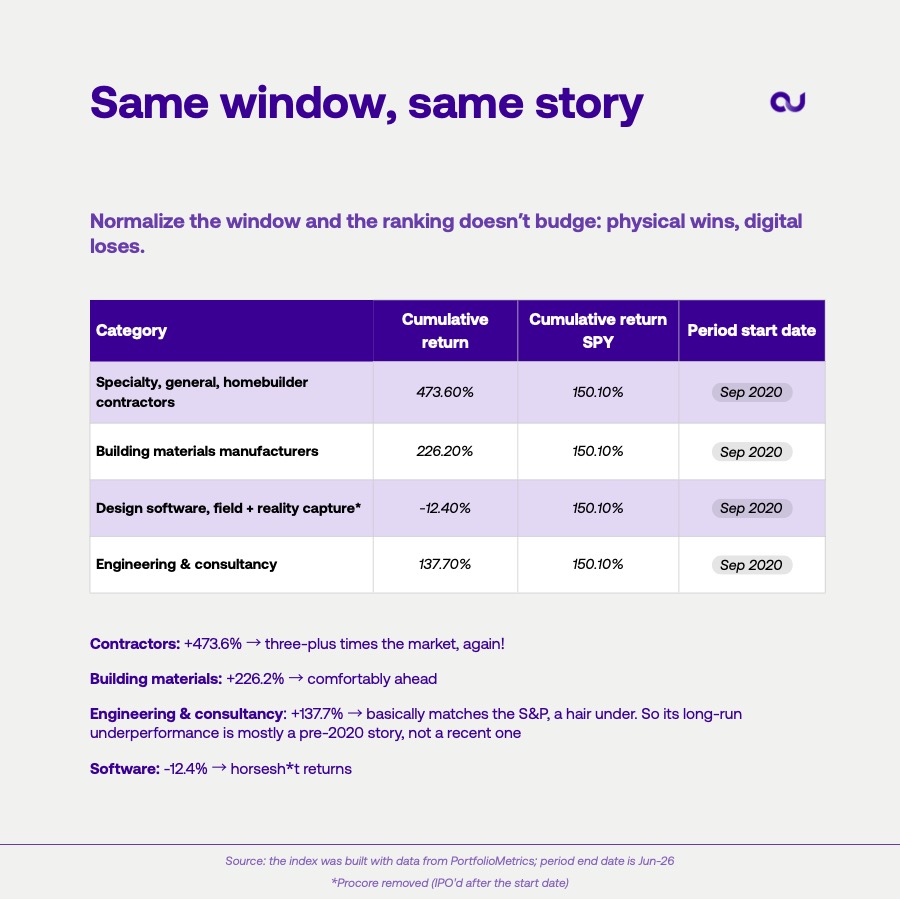

I built some indexes tracking the listed companies of the project economy (contractors, building materials, AEC services, and design software) and ran them against the S&P 500. Over a clean, common window:

• Contractors: +473.6% vs. the S&P's +150.1% → three-plus times the market

• Building materials: +226.2% → comfortably ahead

• Design software: -12.4% → would have been better to invest in a savings account

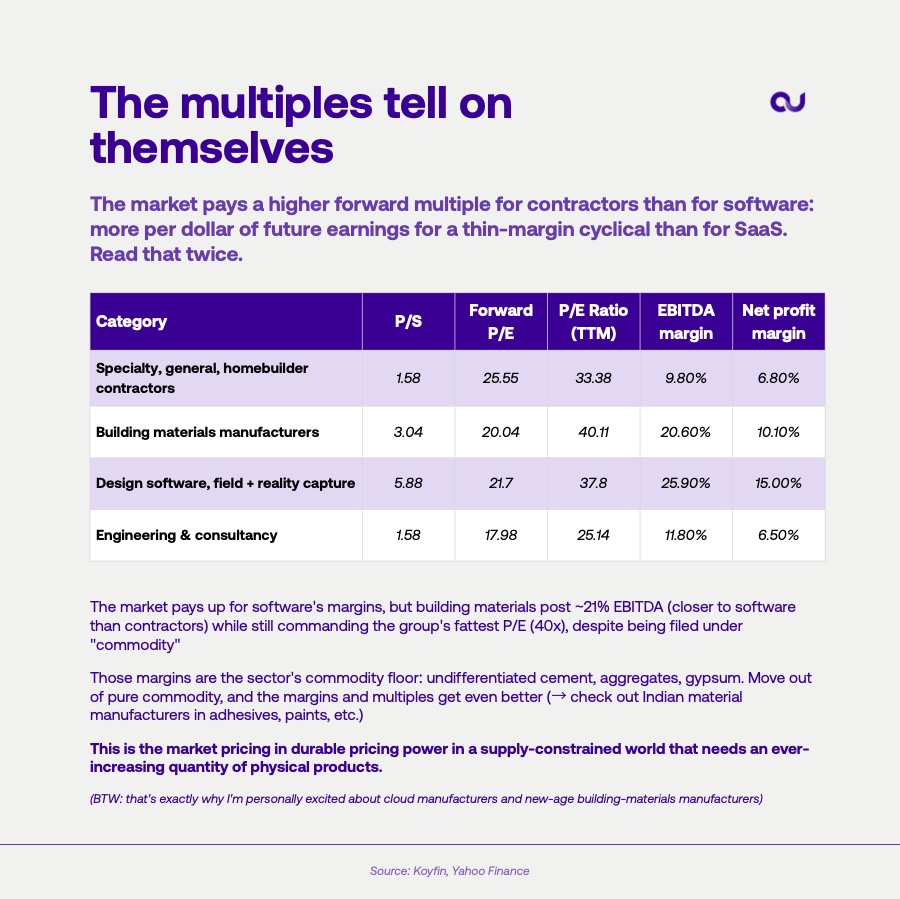

The segment that carries the richest multiples (~6x sales vs. 1.6x for contractors) has lost money for public investors while the "boring" physical businesses ran away with it.

And it's not just the returns. Look under the hood (margins, ROIC, cash yield, even what the market pays for future earnings), and every indicator points the same way: the boring physical businesses are simply the "better" businesses.

The takeaway isn't "software is bad”. It's that the value in this sector accrues where technology touches the physical operations (the deployment, the working capital, the capital efficiency), not in the pure-software layer. Or at least, that’s how I interpret it (I have a personal bias towards ops-intensive business over SaaS, tough!).

Curious to get your thoughts in the comments!