People read Katerra’s collapse as a SoftBank story or from Brian Potter’s infamous article. Big check, bigger ego, predictable ending but that reading is lazy. To me the more interesting story is what happens after the lights go out: who walks the factory floor, who decides which $100m of equipment is worth $20m and which is worth scrap, and who actually has to make modules roll off a line in California with somebody else’s half-finished automation cells.

Michael Palmer ran that process. At the time he was at Volumetric Building Companies (VBC), the modular builder that bought Katerra’s California assets out of bankruptcy in August 2021. He’s now a Partner at Great Wave Ventures, where he invests in the same construction and industrial tech category from the other side of the table. Before VBC he was at Sidewalk Labs working on high-rise prefab mass timber, and before that at Dow running new building-product development and commercialization. He’s an architectural engineer by training turned investor.

I wanted his story because most VC-side commentary on Katerra is a meme. Michael’s commentary is a receipt, besides showing a blatant example of how to acquire failed assets.

“It hasn’t been because they didn’t have enough cash”

Jacopo: Before we get into the deal, give me your read on why Katerra died. The consensus reading is “SoftBank threw too much money at a bad business.” Is that right?

Michael: They raised over $3bn and spent it in less than three years, which is a crazy rise and fall by any measure. But they weren’t focused on real estate, they were buying general contractors, which probably wasn’t the right move to begin with. The thinking was, “we just need to throw cash at this, it doesn’t need to be profitable.” And there was a bit of Silicon Valley hubris in it too, which I myself embodied coming from Sidewalk into VBC: “we can fix this with tech and automation.”

There’s real physics and manufacturing discipline that needs to be incorporated into these businesses, and the majority of the ones that have struggled or failed didn’t fail because they ran out of cash. They failed because they didn’t really understand the business they were starting.

Jacopo: This is the line I keep underlining. It actually maps onto the prefab capital cycle, if you think about it. If you look at VC inflows into prefab, the peak was right before and right after Katerra’s collapse. Maybe the bet was just too early. Or maybe it was always the wrong shape of capital pointed at the wrong shape of problem.

Michael: It was the wrong shape. Cash doesn’t fix unit economics, it just lets you hide them for longer.

Jacopo: How bad were the unit economics, concretely?

Michael: When you walked the factory, the highest level of utilization Katerra was achieving on any individual line was about 15-20%, so they weren’t breaking even on anything. They’d built a cabinet line, a window line, truss lines, things that aren’t really needed for modular manufacturing, and they were trying to keep all of it in house. You had super-automated equipment running at single-digit-teens utilization, which is just a fixed-cost contribution problem the revenue can’t catch.

How the deal actually got financed

Jacopo: How did this even land on your desk? You’re at VBC, an early stage modular company with a single East Coast factory. Not exactly a natural buyer for $100m of equipment.

Michael: We had too much demand, which is the part removed from the narrative. COVID rates went to zero, supply chain shortages were at an all-time high, and modular was suddenly the best way to build. We had domestic supply built up, skilled labor under contract, we were deemed essential, and we could lay out the factory so people weren’t transmitting Covid to each other. The demand we saw was honestly really cool to behold, and very validating.

So we were already planning to raise to expand manufacturing when the Katerra opportunity came across our desk, through our investment partners who happened to have a relationship with SoftBank. Vaughan (our CEO) and I knew exactly who Katerra was, and honestly, I didn’t think we’d get it.

Jacopo: Walk me through the financing structure. This is the part hard tech founders almost never see.

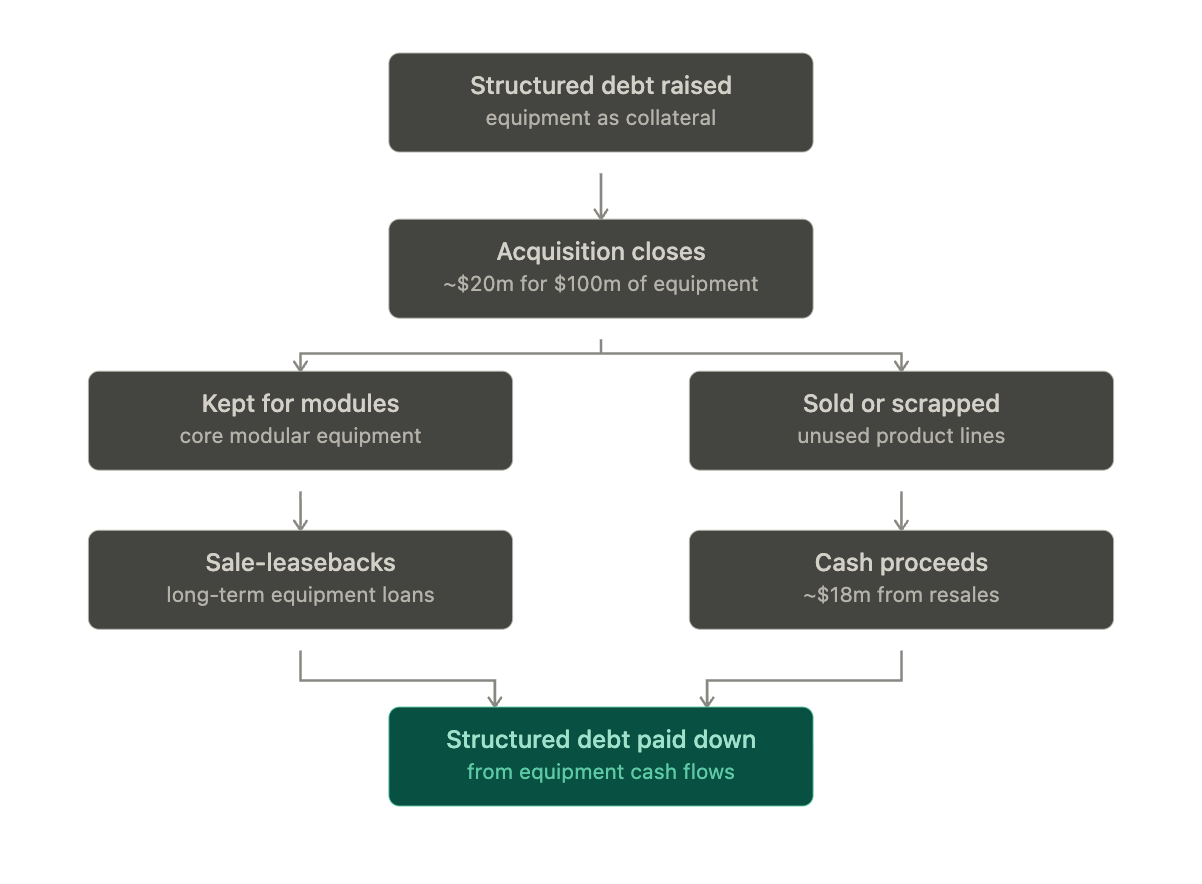

Michael: Our investors said, look, if we buy these assets, it’s all collateral. Let’s structure this as debt and then refinance afterward into an equipment loan.

So the entire acquisition was done on structured debt, not equity. Then my job on the back end was equipment sales: figure out which cells were valuable, which were scrap, and set up the longer term financing through capital leases and sale-leasebacks on the equipment we were keeping. That’s how we paid the structured debt down.

Jacopo: They didn’t issue equity to buy $100m of hard assets. They used the assets as collateral, took on debt against them, and then refinanced into equipment-specific facilities once they knew what was actually keepable. The capital structure followed the physics of what they bought, which is the entire game. And the thing I find absurd is how hidden this is. Most hard tech founders default to equity for everything because they think debt is for banks and banks won’t underwrite them, while there’s a whole stack of asset-backed structures sitting right there.

Michael: We had a very sophisticated CFO at VBC, a tenured person who’d taken companies public, and it was still really hard. That’s the real limiting factor. It’s not that it can’t be done, it’s that doing it is still pretty difficult, and there’s a degree of sophistication required that’s separate from the technological sophistication you expect a founder to have to build a great product.

So as an investor, the question I sit with now is: how do you structure VC-like returns with a creative capital mix in hardware? Because the loudest pushback I hear from other investors is “we don’t do hardware, it’s too dilutive, it requires way too much capital to be raised.”

What you’re actually buying when you buy $100m of robots

Jacopo: There’s always this question with distressed assets: what am I actually buying? Walk me through what Katerra’s $100m of equipment really was, and how it got valued.

Michael: Katerra raised so much money that there was a formal valuation and appraisal already done on every asset, so a starting number existed. The challenge was what wasn’t on the appraisal.

A lot of these cells were custom equipment built by system integrators specifically for Katerra, and Katerra had never paid them. So a vendor would tell me, “you own this piece of equipment, but technically you don’t, because I’m still owed $600k.” Through bankruptcy that’s not legally relevant, but it is operationally relevant, because the equipment doesn’t work and I need the integrator to make it work if I’m going to keep it. Which means I need a master service agreement, or some commitment that they’ll get it running.

There were dozens of automation cells in that facility, spread over more than ten different product lines. Some of those cells were flat-out never going to work, so we just scrapped them and priced the acquisition that way. Other ones we negotiated MSAs back into.

Jacopo: How did the due diligence actually take place?

Michael: Katerra declared bankruptcy on June 21st, and we had keys to the kingdom on August 16th, so roughly six weeks. Vaughan and I genuinely didn’t sleep through any of it, because we had 15-minute calls set up back to back, renegotiating every single contract through the bankruptcy process before close, so we’d actually understand what we were buying. It was insane.

I flew out on August 16th and there were two cars in the parking lot, the facility maintenance guy and a technician. People literally still had lunches sitting on their desks from when Katerra let them go.

The tribal knowledge is the asset

Jacopo: I want to push on something. You mentioned hiring people back from Katerra. That feels under-discussed in fire sale conversations. We always talk about the equipment. Nobody talks about the operating knowledge.

Michael: It’s not like you just buy a Toyota Camry and they’re all more or less the same and you can swap parts. Each of these machines is bespoke, shipped halfway across the world, and things happen in transit. There’s a history with every cell, like, “did you buy a lemon? This one always breaks saw blades because of some weird inconsistency we can’t figure out. The maintenance logs here have us constantly changing the oil for this particular machine, and one time we didn’t do it for three months and then we had this huge shutdown, so now we’ve got this other thing that’s a lasting consequence of that.”

You can’t get that from documentation. You get it from the people who ran the machine.

So we ended up hiring probably half of the Katerra people we encountered through that process, not as a charity move but because they were the asset. The robots without them were partially scrap.

Jacopo: So it’s not really about acquiring failed assets. It’s about acquiring the tribal knowledge attached to the failed assets.

Michael: Right. And it’s also worth saying about Katerra specifically that those were smart people who genuinely thought they were changing the world. I saw the same thing at Sidewalk: people who thought, “I believe cities can be better, I believe we can do affordable housing better.” At VBC the same. At Katerra the same. The company got so big so fast that the good ideas got buried in the sauce, but they were there.

If I were sitting in a room with a Katerra C-level today, I think the question they’d ask me is: which things actually worked? Because there were real successes ones.

The balance sheet was great. The income statement was the challenge.

Jacopo: From a balance sheet perspective, you guys must have been thrilled. $100m of equipment at 10 cents on the dollar.

Michael: Balance sheet was great. The challenge was the income statement. We had a ton of assets but no immediate revenue against them, and we had to enter a new market on top of that. California building codes are completely different from the East Coast, so we basically had to build a new modular product, set up new customer relationships, and do all of that at a scale that was unnecessarily large for what a greenfield entry should be.

Nobody in their right mind would build that size of facility to enter the California market. You’d build something with option value so you could expand the footprint, unless you have $3bn sitting around, in which case the calculus changes.

We bought it in August 2021, and by probably early Q2 2022 we were producing our first module. That’s the gap you have to solve for.

Jacopo: How did you actually fill in the operating mix? You couldn’t run Katerra’s footprint as-is.

Michael: We kept the things that were actually needed to build modules: Homag, Weinmann saw lines, an Auto-wall line, the cabinetry line, some wood-panelized systems, and racks for transporting wall panels. We sold off everything else.

Then we imported equipment from Europe to retrofit the facility for modular, with a Swedish team on the ground helping us commission it. In hindsight, we probably could have done some more manual things in the early days just to get up and running, because we increased the fixed-cost base before the revenue ramped. That just added pressure that probably didn’t need to be there.

For VBC, though, it ended up being one of the more important things we ever did. It made the business national, because we could service any state out of either factory. From North Carolina we were able to ship modules to Denver economically and still pencil, which gives you a sense of the economic shipping radius once your unit economics work.

California specifically has the highest demand for affordable housing in the country, and we did a ton of supportive housing and student housing out of that facility. Decent margins because the cost to build there is so high, and we were located close enough that our shipping was super competitive against anyone trying to ship in from out of state.

On top of that, we acquired a Polish company called Polcom that builds high-rise steel modules, which let us go up to 22 stories. So over an 18-month stretch we bought Katerra, relocated our North Carolina facility up to Berwick, Pennsylvania, and added Polcom, all while ramping three factories at once.

I would not wish that on my worst enemy. But the financing creativity and operational discipline it forced on us was pretty cool.

Any framework out of this chat? Yes!

A few things I’m taking out of this conversation, written down so you don’t have to.

- The cash didn’t kill Katerra, the missing manufacturing discipline did.Every prefab failure I’ve looked at rhymes - the diagnostic is utilization on the line and revenue against installed fixed cost, not capital raised.

- something we keep repeating at Foundamental is: prefab hasn’t been working at scale because it standardizes around supply, but the most basic unit of supply in construction are standardized already (eg bricks, 2-by-4, steel rebars). Why not standardize around demand instead?

- Distressed asset deals should be financed against the assets, not the equity. VBC’s acquisition was structured as debt, collateralized by the equipment, with a path to refinance into equipment loans and sale-leasebacks once scrap-vs-keep was sorted. If you have to issue dilutive equity to buy hard assets at a discount, you’re doing it wrong.

- The appraisal is a starting point. What the appraisal won’t tell you: which integrator relationships are strained, which cells were custom-built and now unable to be supported, which lines are economically dead even if mechanically alive. Bake the messy version into the bid.

- The operators are part of the asset. Tribal knowledge on automation cells does not survive a bankruptcy filing. If you’re underwriting a distressed industrial deal and you haven’t budgeted to rehire the people, you’re modeling a worse asset than you think you’re buying.

- Buying an automation cell does not mean it works. Each piece of equipment has a history. Saw blades, maintenance gaps, transit damage, integrator disputes. Plan for a per-cell MSA process, not a clean handoff.

- Balance sheet wins don’t pay payroll. A 10-cents-on-the-dollar acquisition is still a fixed cost ramp. The relevant question is how you finance the gap to first revenue, rather than how good the headline price was.

- The capital-structure problem in hardware is sophistication. Per Michael, even a tenured CFO who’s taken companies public found this hard.

- that’s the gap most founders fall into, and it’s the thesis behind the financing tool I’ve been building. If you missed it, the previous episode of this series sits next to this one nicely: I sat down with William Godfrey of Tangible to walk through the actual mechanics of debt vs. equity for hard tech. This conversation with Michael is what that one looks like applied to a real $100m deal.

Thanks to Michael for being generous with his time and for being unusually direct about what worked, what didn’t, and what he’d do differently. If you’re an operator or investor working in this space and want to be a guest, hit reply.